Towards a systematic approach to private sector engagement

A thought exercise

The United Nations remains at its core an intergovernmental organization, but contemporary challenges cannot be solved by governments alone; they also require the engagement of the private sector, particularly in emerging domains such as artificial intelligence. The United Nations already has formal mechanisms through which to engage with the private sector, including through frameworks such as the Global Compact and through individual partnership agreements, which are focused on coordination and implementation. But the private sector is largely excluded from most systematic analysis and decision-making processes at the United Nations.

Another reason for engaging the private sector is, of course, the fact that—in addition to the technical expertise that they possess—companies also have considerable financial resources. In 2024, the private sector provided nearly $574 million in voluntary contributions to the United Nations system, of which the Secretariat received over $152 million.1 Being able to more systematically tap into such a source of funding is badly needed at a time when the Secretariat faces potential financial collapse and amidst historic declines in official development assistance.

However, increasing reliance on private sector funding under existing arrangements creates a significant risk of organizational capture. The literature already demonstrates how earmarked voluntary contributions from member states can divert international organizations from intergovernmentally agreed mandates and priorities.2 I would argue that the risk is higher from the private sector than from donor countries, given that funding is the primary way that corporations can influence the work of the United Nations given that they are excluded from formal participation in the main organs, unlike member state donors.

One potential way to square this circle is to engage private sector organizations in the work of the General Assembly in a manner similar to the arrangements in place for observer states.

Observer states

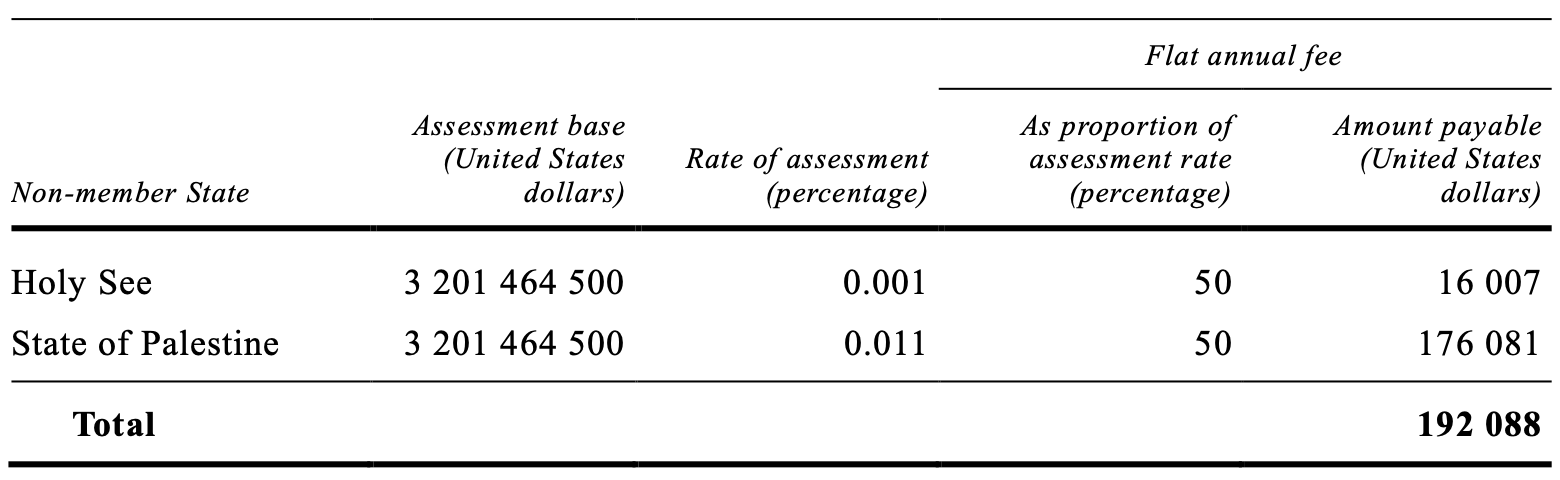

Non-member states have been allowed to participate as observers in the General Assembly since 1946 when the Swiss government was given observer status.3 Today, non-member states are granted observer status by the General Assembly through the adoption of a resolution; the most recent example is the State of Palestine, which was granted status in 2012 through the adoption of resolution 67/19. Non-member states are extended a range of rights and privileges regarding participation in the work of the General Assembly but do not have the right to vote.4

In exchange for observer status, non-member states have to pay a flat rate to the United Nations,5 which is currently set at 50% of a notional assessment rate calculated based on their national income data.6 The two current observer states, the Holy See and Palestine, have notional rates of assessment of 0.001% and 0.011%, respectively and are charged half that level.

An important aspect to note is the fact that the fees charged to non-member states is supplemental to, rather than a share of, the budget. In other words, funding provided by non-member states helps fill the gap in funding resulting from member states not paying their assessed contributions in full.

How this could work

The same procedures that apply to non-member states seeking an arrangement akin observer status could be applied mutatis mutandis to private sector entities seeking greater engagement with the United Nations. This would include the granting of status through a decision of the General Assembly—which would have to specify which subset of rights and privileges of participation would be extended to such entities—along with the charging of an annual fee. The exact same approach need not be taken given how different corporation are from states, but the approach used for observer states gives us a starting point for thinking about how a more systematic approach could work. Of course, the General Assembly should decide on eligibility criteria and arrangements to ensure regional and sectoral diversity, and ways to keep the number of private sector participants manageable, whether through a hard cap, term limits, rotational scheme, or other methods.

The notional assessment rates for non-member states are currently calculated using their national income data. Obviously, there is no perfect gross national income analogue for private sector entities, but revenue could potentially work as a basis for calculation of a notional assessment rate. The top 50 companies by revenue in the Fortune 500 list had revenues ranging from between $150 to over $700 billion in 2024.7 If revenue were used to calculate nominal assessment rates for 2026, fees for the top 50 companies would range from $2 and $10 million each. This is not a game-changing amount—it’s certainly not a solution to the current financial crisis, and nor should it be pursued as such, even if the funds collected in this manner would help relieve funding shortfalls and liquidity challenges.

Of course, if member states want to go down this route, they can choose different ways to calculate the nominal assessment rate and whether to apply the 50% adjustment—or set a different rate—that currently applies to non-member states. After all, it is not difficult to imagine different arguments for different arrangements based on considerations such as the capacity to pay (the principle underpinning the scale of assessments) and the subset of rights and responsibilities to be extended.

Final thoughts

Let me underline that this is a thought experiment. Even if adopted, this framework would need to be part of a broader strategy that also incorporates and more systematically leverages existing arrangements for private sector engagement such as the Global Compact and partnership agreements. But perhaps this thought experiment can help kickstart a conversation about how to find a structured way for private sector entities to more systematically contribute to and participate in the work of the United Nations and to have a transparent, predictable, and accountable way of providing resources, all while mitigating the risk of organizational capture by keeping decision-making and oversight within the hands of member states.

© 2026 Eugene Chen under CC BY-NC-ND 4.0

The views expressed herein are those of the author and do not necessarily reflect the views of the United Nations University.

United Nations System Chief Executives Board for Coordination. (n.d.). Financial Statistics Database [Dataset]. https://unsceb.org/financial-statistics

Graham, E. R. (2023). Transforming international institutions: How money quietly sidelined multilateralism at the United Nations. Oxford University Press. https://doi.org/10.193/oso/9780198877936.001.0001

United Nations (1946). Negotiations with the Swiss Federal Council: Report of the Secretary-General (A/175). https://undocs.org/en/A/175

For a list of rights and responsibilities extended to non-member states, see the annex to United Nations General Assembly (2003): Resolution 58/314. Participation of the Holy See in the work of the United Nations. https://undocs.org/en/A/RES/58/314

United Nations General Assembly (1989). Resolution 44/197 B. Scale of assessments for the apportionment of the expenses of the United Nations. https://undocs.org/en/A/RES/44/197

United Nations General Assembly (2003). Resolution 58/1 B. Scale of assessments for the apportionment of the expenses of the United Nations. https://undocs.org/en/A/RES/58/1B

By way of comparison, UN member states with gross national incomes of comparable levels roughly fell between the 70th and 90th percentiles, with assessment rates ranging from 0.149 for Slovakia to 0.773 for Belgium.

Have you thought about the NGO Committee process? It's a hornet's nest but there are criteria and review process already and certain rights accorded.